URGENT Update – Steel Market Conditions

As you are no doubt aware, the steel industry is currently experiencing significant disruption on multiple fronts. While escalating tensions in the Middle East are a major contributing factor—driving energy market instability and cost inflation—the wider situation is more complex and is likely to have broader, longer-term implications for global supply chains.

Recent reporting highlights how energy shocks linked to geopolitical tensions are already feeding through into construction and steel pricing, compounding an already fragile market environment.

Steel supply problems

The recent conflict has already had an immediate effect on oil, gas, and freight costs, creating increased volatility across the market. This has resulted in several mills temporarily withdrawing from supply, placing additional pressure on both availability and pricing throughout the supply chain.

Industry sources confirm that energy-driven cost increases and global trade disruption are tightening supply, with contractors warning that rising material costs are being amplified by wider geopolitical instability.

At the same time, global protectionist policies and shifting trade flows are reducing the availability of imported steel, with buyers having nowhere to turn, as domestic supply simply cannot meet the 40% reduced shortfall on imports – amid impending tariff risks, quotas – due on July 1st, resulting in higher prices and longer lead times.

Logistically, the affects on shipping, transport from the far east will not be solved quickly – months of disruptions lay ahead with dramatically reduced imported stock due to EU & UK protectionism.

EU Tariffs and UK safeguarding

Looking ahead, the market faces further uncertainty as governments move to protect domestic steel industries.

In the UK, the Government has announced a major shift in policy, including reducing import quotas and increasing tariffs to 50% on steel entering outside those quotas, alongside a target to produce up to 50% of domestic steel demand.

Similarly, the European Union is proposing significant reductions in tariff-free import quotas, with tariffs also rising to around 50%, in an effort to shield its own steel sector from global oversupply.

These measures reflect a broader global trend toward protectionism, as countries respond to excess supply and subsidised exports from major producers.

However, there is growing concern within industry that such policies—while supporting domestic mills—may further restrict supply and increase costs for manufacturers and end users.

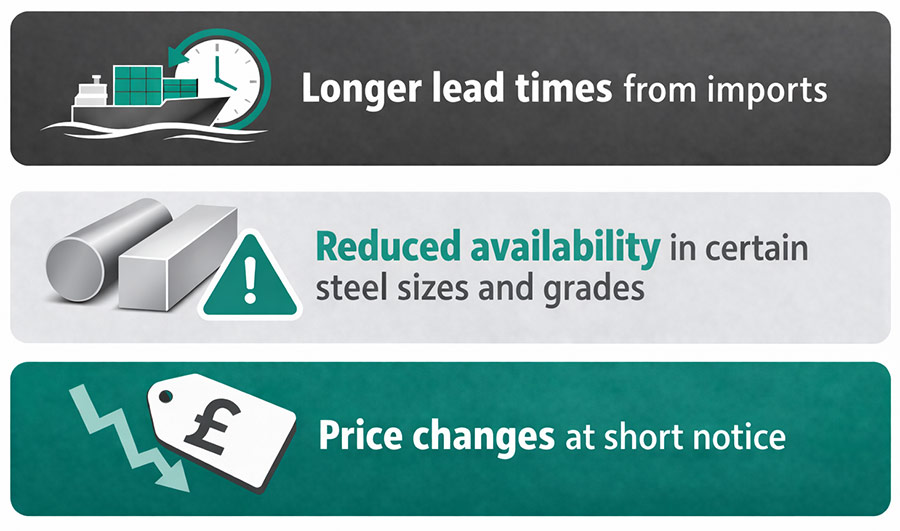

Market effects

Based on current information from mills, manufacturers, and stockholders, we are observing:

- Lengthening lead times on certain products

- Reduced availability across some sizes and grades

- Increased price volatility, often at short notice

Analyst forecast

For stockholders and engineering firms, this means:

For stockholders and engineering firms, this means:

Market analysts are already forecasting significant price increases throughout 2026, driven by reduced quotas, 50% tariffs, reduced imports. Then from January 2027 the introduction of carbon border measures (CBAM), and reduced imports.

At the same time, industry leaders are warning that rising costs and restricted imports could place additional pressure on downstream manufacturers and construction projects.

There is a deeper contradiction in the government’s approach.

- UK steel assets are already heavily supported by public funds

- Major players like British Steel and Tata have received significant tax payer backing

- Ownership structures are often international (Chinese, Indian)

The outlook for steel markets

We expect these pressures to continue (and potentially intensify) over the coming weeks and months as:

- Energy markets remain volatile

- Trade restrictions tighten across the UK, EU, and globally

- Supply chains continue to rebalance toward domestic sourcing

As always, we will continue to monitor developments closely and keep you informed.

For customers requiring engineering-grade materials such as EN9 and EN19 black flat bar, we continue to support supply wherever possible despite current market pressures.

To discuss any challenges you may be facing in supply, or to discuss how High Peak Steels can support you at this critical time call us directly on 01457 866911.